A Breakthrough in Arctic Trade Routes

The Arctic is Melting

Polar caps in the Arctic are receding, creating access to new trade routes for parts of the year. The routes are valuable short cuts for global trade but the waterways are precarious to navigate with unpredictable weather, the need for specialized icebreaking ships, and the necessity to operate at slower speeds, all of which make the routes less commercially reliable and partially offset the savings in time and fuel. But the waterways are highly strategic economically, politically, and militarily, which is why the U.S. Navy is updating its Arctic Strategy, why China has drawn up a Polar Silk Road whitepaper, and why Russia seeks to solidify its control of, and successfully monetize, the route that traverses 3,000 nautical miles along its northern coastline. Here’s your Arctic Trade 101 on the opportunities and challenges ahead in expanding use of the Arctic waterways.

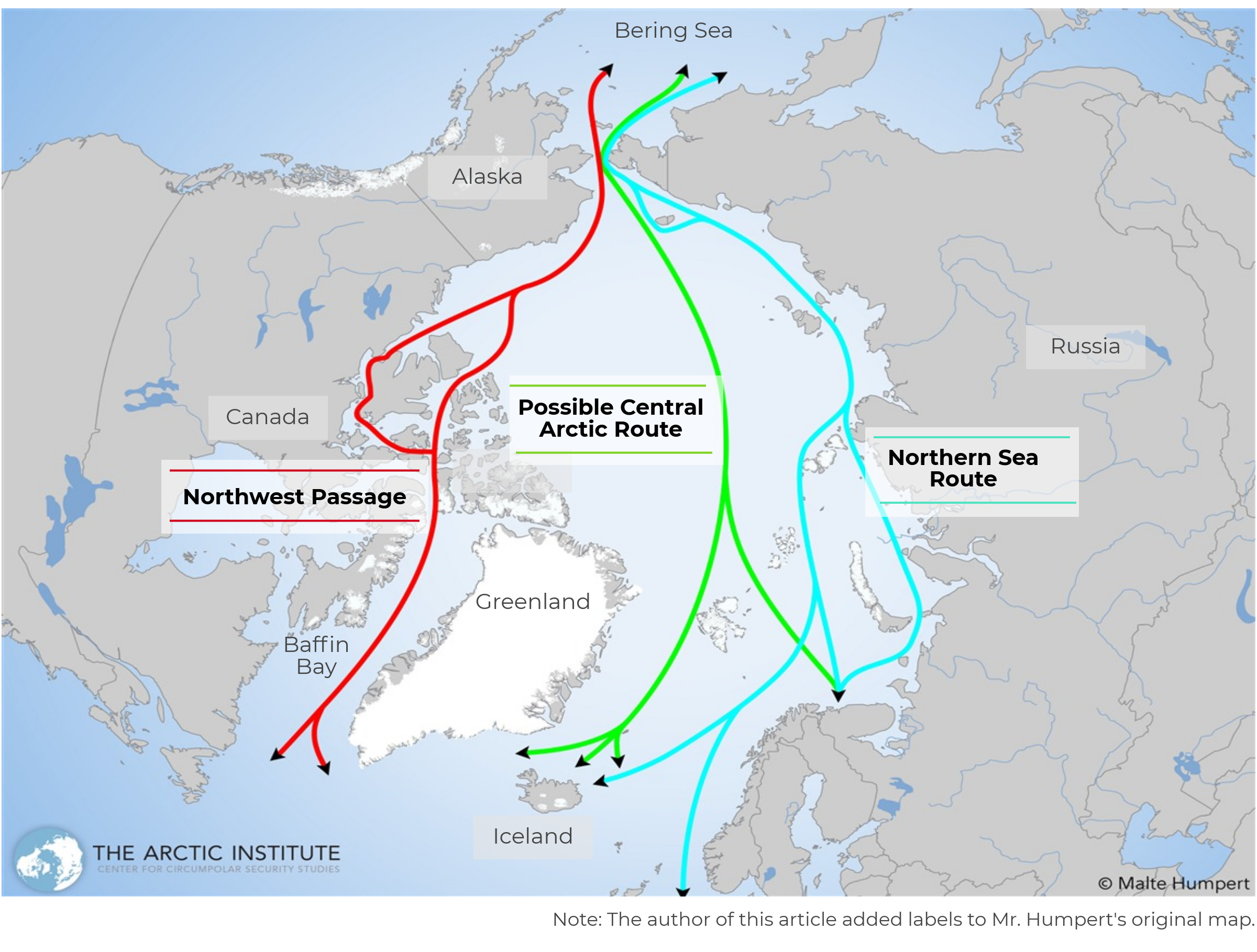

The Trans-Arctic Routes

Three trade routes run through the Arctic. The Northwest Passage runs along the Canadian and Alaskan coastlines from Baffin Bay near Greenland to the Bering Strait between Alaska and Russia. The Northern Sea Route is a national waterway of the Russian Federation that crosses seven time zones as it wends its way along Russia’s coastline. The Central Arctic Route is the shortest possible route connecting the Pacific and Atlantic Oceans, running from Iceland straight through the Arctic Circle over the North Pole to the Bering Strait, but this route is still constrained by thick ice caps; experts forecast it could be navigable by around 2050.

Though there are multifaceted reasons for Arctic stakeholders to invest in the development of these routes and to debate their governance, the commercial trade opportunity comes down to saving time and money transporting cargo. By way of example, Arctic Portal analysts estimate that a medium-sized bulk carrier using the Northern Sea Route could save 18 days, 540 tons of fuel, and between 180,000 and 300,000 euros for a trip from Norway to China versus the alternative route from Europe to Asia through the Suez Canal.

Who Has a Stake in the Arctic Routes?

The Arctic Council is the primary organization for international cooperation on arctic exploration and development. Its permanent members are countries that have territory on, or in the vicinity of, the arctic circle (those are “near Arctic states”). Members include the United States, Canada, Russia, Finland, Denmark, Iceland, Norway, and Sweden. But other countries have significant interest in the arctic whether for environmental and conservation reasons, national security concerns, or because the arctic is home to significant natural resources in addition to potentially valuable sea routes for cargo. For these reasons, the Arctic Council has official observers (self-designated “Arctic stakeholders”) that include China, France, Germany, Italy, Japan, Netherlands, Poland, India, Korea, Singapore, Spain, Switzerland, and the United Kingdom.

Other regional organizations play a role in shaping the geopolitics and cooperation on arctic policy, such as the Barents Euro-Arctic Council, which works on environment, transport, rescue, and economic cooperation issues as well as the preservation of indigenous culture, and the cultivation of tourism.

Russia Needs to Ship Its Natural Resources

China and Russia emerge as two dominant actors in the race to develop, control, and use these waterways. Russia’s primary economic opportunity in Arctic thawing lies in improved access to minerals, oil and gas, and other valuable natural resources that can be extracted and more easily moved internally to its ports. The United State Geologic Survey estimates that 13 percent of global oil and thirty percent of natural gas are in the Arctic, much of it in Russia. Russia is also sitting on metals critical to the production of electronics and other technologies, including nickel, palladium, platinum and copper.

Russia continues to build ports along the Northern Sea Route, which they can use to transport natural resources to Europe year-round and to Asia for extended months over the summer, and has developed a fleet of LNG carriers for the task that do not require the assistance of icebreaking escorts – the world’s first such ships made by Korea’s Daewoo Shipbuilding, capable of carrying 170,000 cubic meters of LNG. While exploiting the Northern Sea Route to move its own cargo, Russia could also create a lucrative maritime toll road, charging Chinese and other carriers premiums to use the route.

China’s “Polar Silk Road”

China is also making direct investments in oil and gas and mineral industries throughout the region, as well as in the development of ports in Arctic states, so that it can both diversify its energy sources and better control the means to transport them. The value of its cargo moving along Arctic routes is thus far relatively low, but the Polar Research Institute of China forecasts that as much as 5 to 15 percent of China’s trade by value could move through the Arctic by 2020.

Redirecting a portion of its commerce to Arctic routes also helps China reduce its dependence on the Strait of Malacca, where there is a U.S. naval presence. Over 64 percent of China’s maritime trade transited the South China Sea in 2016, mainly through the Strait of Malacca. China is monitoring Arctic melting from satellites, and building its own fleet for the Arctic; its next icebreaker, the Xuelong 2 will be ready for delivery in 2019, around a year before the United States begins construction of its next icebreaker. China is closely watching the navigability of the Central Arctic Route, which would allow it to avoid the Russian-controlled route.

Will Arctic Shipping Break Through or Develop at a Glacial Pace?

These routes offer a shortcut that can save time and money in fuel, but navigation is still risky and requires more expensive ships to break the sea ice, which means premium shipping fees and higher insurance costs. Icebreakers capable of moving through ice up to four feet thick will still be required until around 2045 when the ice will be thin enough for cargo ships to get through. It can be difficult to predict when navigable conditions will begin and end each season. Even during the summer shipping season, weather is challenging and variable with the potential for high winds and low visibility.

Given these constraints, the Arctic routes are better suited to moving bulk tonnage – oil and gas and dry commodities like iron ore – than for container goods shipping on just-in-time schedules. Thus, despite the interest in their use, only around two percent of global shipping could be diverted to these routes in the near term; perhaps up to five percent by 2030.

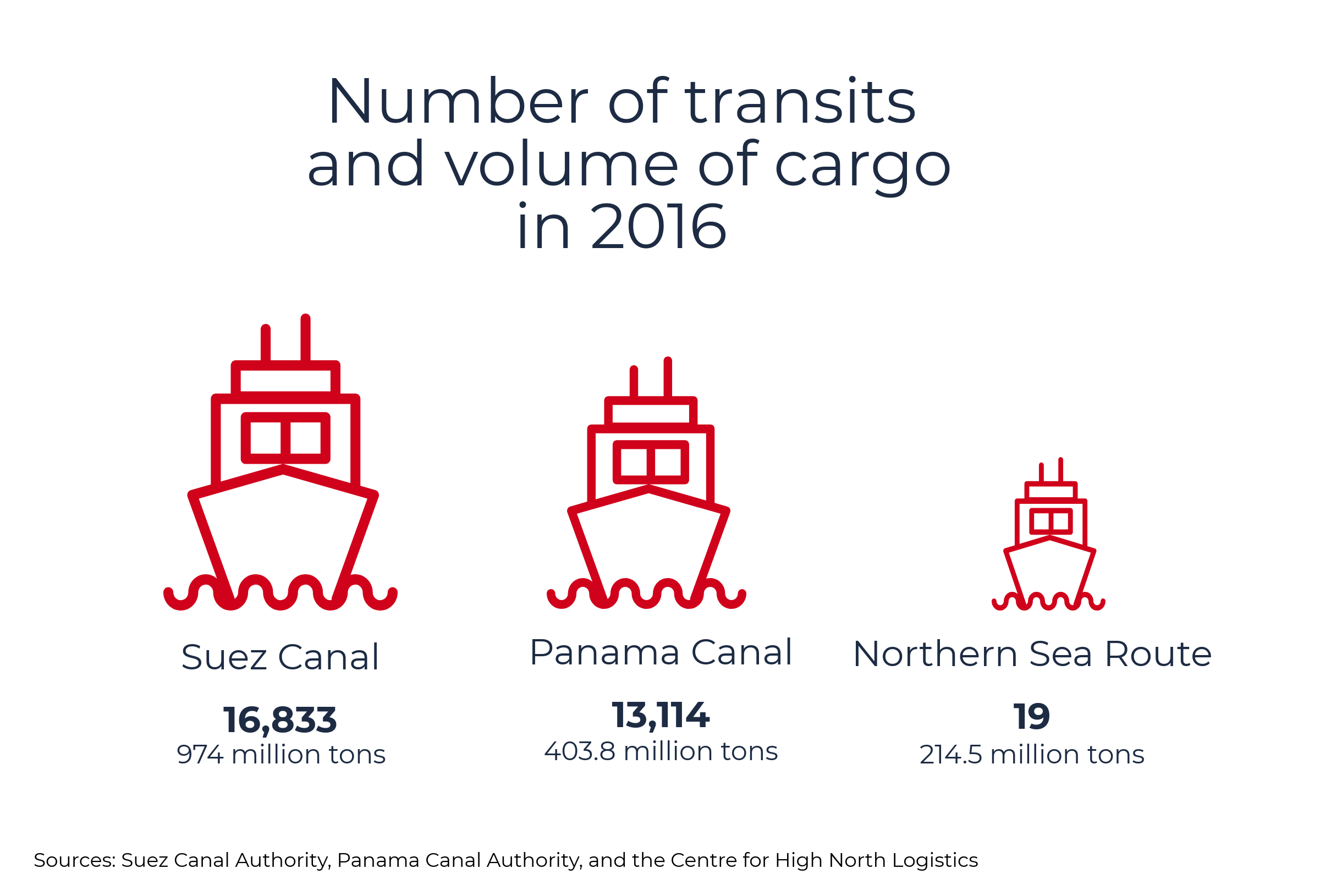

How much more cargo trade ultimately traverses the Arctic will depends on how fast the ice melts, demand for natural resources, global shipbuilding capacity, and other factors such what fees Russia may decide to charge for its route. Transits on the Northern Sea Route have been growing but from a relative low of 19 vessels in 2016, compared with around 16,800 transits of the Suez Canal and 13,100 transits of the Panama Canal in 2016.

It is remarkable these ships can manage at all in such inhospitable and dangerous conditions. And for now, while global powers ramp up their capabilities and sort out maritime codes and governance of these waterways, the Arctic routes will remain merely supplemental to the world’s main canals and trade waterways.

Andrew Lepczyk is candidate for masters degree in international economics at American University and served as a research intern for the Scholl Chair at CSIS.

Leave a Reply

Want to join the discussion?Feel free to contribute!