Are Quotas Worse Than Tariffs?

Quotas Return

With all the focus on tariffs these days, it is easy to overlook the return of another tool used to limit imports: quotas.

Over a year ago, the Trump Administration used Section 232 of the Trade Expansion Act of 1962 to impose 25 percent tariffs on specified steel imports and 10 percent tariffs on specified aluminum imports. Three countries – South Korea, Brazil and Argentina – made agreements with the United States to apply quotas to their steel exports in lieu of the Section 232 tariffs. Argentina also agreed to quotas on its aluminum exports.

According to numerous reports, U.S. negotiators were seeking similar agreements with Canada, Mexico, Japan and the European Union (EU). In May 2019, however, the governments of the United States, Canada and Mexico announced that they had reached a deal to lift steel and aluminum tariffs without imposing quotas, choosing instead to adopt a monitoring system with the right to re-impose tariffs on these products if surges are detected in the future. This deal could be a template for agreements with Japan and the EU to address their steel and aluminum tariffs.

In ongoing Section 232 investigations, the administration is keeping quotas on the table in other sectors including autos and auto parts, uranium ore and titanium sponges.

The Difference between Quotas and Tariffs

Quotas and tariffs are both used to protect domestic industries by artificially raising prices in the domestic market. Their administration and effects, however, differ in specific ways. Quotas restrict the quantity of a good imported from another country. Tariffs are a charge levied on the value of goods imported from another country.

While tariffs generate revenue that is paid to the importing country’s treasury, the value of a quota, also called “quota rents,” generally goes to the foreign exporters who are able to sell goods subject to the quota at higher prices and collect higher per unit revenue. In both cases, domestic consumers in the importing country pay the costs of tariffs and quota rents. But with quotas, the government of the importing country receives no revenue.

Quotas can be much more complicated to administer than tariffs. Tariffs are collected by a customs authority as goods enter a country. With quotas, customs authorities must either monitor imports directly to ensure that no goods above the quota amount are imported, or can award licenses to specific companies, giving them the right to import the amount allowed under the quota. Quotas can also take the form of a voluntary export restraint (VER), where the exporting country administers the quota.

The Cost of Quotas

Costs and pricing under a tariff regime are more transparent and predictable compared to quotas. For example, if a good is subject to a 10 percent tariff, then the good should cost about 10 percent more than it did before the tariff was imposed. With a quota, the price of that same good can increase as long as demand for the good continues and the supply remains constrained. This can mean that quota rents are ultimately more costly to domestic consumers than a tariff. In this way, quota regimes may incentivize foreign producers to upgrade the quality of their exports, leading to more direct competition with domestic producers and a higher-price product mix for consumers.

On the other hand, if foreign producers export low quality goods under a quota regime, prices and profits for both foreign and domestic producers of low quality goods will rise because of quotas, while domestic consumers were forced to pay more for lower quality goods.

The General Agreement on Tariffs and Trade (GATT) prohibits quotas and other quantitative restrictions under Article XI (with specific exceptions including for “security reasons”) as the GATT parties agreed that quantitative restrictions were overly restrictive and distortive compared to duties or taxes, where are permitted.

Tricky to Administer

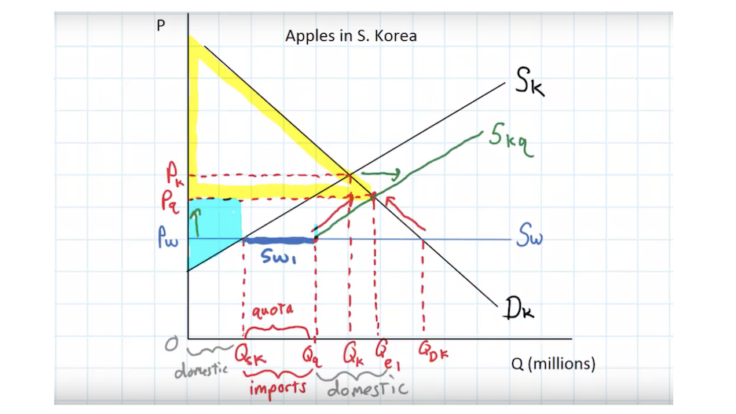

In the case of South Korea, Brazil, and Argentina and Section 232 quotas, each country agreed to product-specific absolute quotas on 54 separate steel articles based on each country’s average annual import volumes of steel from 2015 through 2017. Argentina also accepted product specific absolute quotas on two aluminum product categories.

These quotas are administered by the United States to give exporters the least possible flexibility and demonstrates how complicated quota regimes can be. Some of the quotas are absolute – once the quota is reached, no additional amount can enter the United States for any price, unless an exclusion is granted. Some quotas apply to the full calendar year (but in practice may fill the minute the quota takes effect), and others are subject to quarterly limitations. Once a quota is filled in a given quarter, importers must wait until the next quarter until they can bring the product into the United States.

The True Cost in Practice

For South Korea, Brazil, and Argentina, quotas have reduced export volumes and revenue. According to U.S. Department of Commerce data, the overall quantity of steel South Korea, Brazil, and Argentina exported to the United States in 2018 dropped significantly compared to 2017, by 26.2 percent, 14.6 percent, and 20.1 percent, respectively.

In terms of value, South Korea and Argentina’s steel exports subject to quotas dropped by $430 million and $1 million, respectively, from 2017 to 2018, while the value of Brazil’s steel exports under the quota increased by nearly $145 million in 2018. Argentina’s aluminum exports subject to the quota dropped by approximately 86.8 million kilograms from 2017 to 2018, by 32.8 percent, with a decrease in value of approximately $101 million, according to data from the U.S. International Trade Commission.

Although South Korea, Brazil, and Argentina have benefitted from generally higher prices in the United States for steel and aluminum, so far, the quotas are effectively reducing U.S. imports from these countries.

Upsides for U.S. Steel Producers

For U.S. steel and primary aluminum producers, Section 232 tariffs, and to a limited extent, quotas, are accomplishing their goal of bolstering U.S. manufacturing capacity and allowing their firms to become profitable again — at least in the short run.

Though some proponents of the Section 232 protections do not advocate for quotas specifically, and recognize their downsides, others argue that quotas are a necessary component of the Section 232 program. Here’s why.

First, for industries seeking protection, quotas arguably provide greater certainty than tariffs that imports will be limited. Under tariffs, if importers can bear the costs, or exporters can reduce their prices, imports will continue to flow in and competition will remain high. For example, Vietnam’s 2018 exports of flat steel products, which are covered by Section 232 tariffs, increased by 79 percent compared to 2017. If strict quotas were applied instead of tariffs, Vietnam’s 2018 exports likely would have decreased.

Second, steel and aluminum manufacturers argue that without quotas, “countries that have exemptions [to the Section 232 tariffs] would likely redirect their metals exports to the United States to take advantage of higher prices there, undermining the purpose of the tariffs.”

Finally, the Trump Administration perceives that Section 232 quota agreements with U.S. trading partners and security allies, in combination with tariffs, are helping to pressure and incentivize allies to take seriously the problem of global excess capacity. U.S. unilateral tariffs may also have the opposite effect, though, – making allies less willing to work cooperatively with the United States to address fundamental global problems.

Downsides for Downstream Industries

It’s a different story for U.S. downstream manufacturers, who say quotas have entailed “severe supply constraints” and “created even more business uncertainty than tariffs”.

Importers may no longer be able to guarantee that their goods can enter under the quota, or at all. They may encounter unanticipated costs in the form of storage charges and shipping fees if the quota is filled while goods are in transit. They may face unpredictably higher prices for goods subject to a quota. They may have to find new suppliers and bear all the costs of negotiating new contracts, building new relationships, and shipping from a new location. The exclusion process implemented in August 2018 may provide some relief for importers under supply pressure, though its application may also introduce more uncertainty.

More generally, downstream manufacturers argue that Section 232 quotas and tariffs raise prices inhibiting their competitiveness, and have a chilling effect on growth, employment and investment. Although many businesses have been buoyed by the strong U.S. economy, they say that employment and sales in their industries would have increased even more were it not for tariffs and quotas raising prices. Moreover, downstream industries using steel and aluminum products employ more Americans than steel and primary aluminum manufacturers, so many jobs are vulnerable if supply contracts too much.

North America Alternative to Metal Quotas

In order to move forward with passage of the United States-Mexico-Canada Agreement (USMCA), the United States, Canada and Mexico first had to address the steel, aluminum and retaliatory tariffs in place since 2018. Although all parties considered quotas as a possible way forward, in the end, they agreed to lift all steel, aluminum, and related retaliatory tariffs, as well as withdraw pending WTO litigation, without imposing quotas.

The three countries agreed to prevent the importation of aluminum and steel that is unfairly subsidized and/or sold at dumped prices; prevent the transshipment of aluminum and steel made outside of Canada, Mexico, or the United States to the other country; and establish a monitoring process to detect surges of aluminum and steel imports among them.

This agreement is a positive development for two key reasons: the parties removed tariffs while avoiding quotas, and agreed to address the underlying cause of U.S. industry distress – global excess capacity.

Addressing Global Excess Capacity is Key

Though tariffs and quotas may provide short-term relief, solving underlying global excess capacity problems is critical to addressing U.S. industries’ long-term challenges, and any long-term solution will require more than the mere application of protectionist measures. The United States will have to work closely and creatively with its trading partners to address this challenge directly and to persuade the world’s largest producers — including China — to reduce global excess capacity.

This article is a shortened version of an original report published by the Hinrich Foundation.

Feature Image Credit: Jason Welker, from “Protectionist Quotas” video on Youtube.